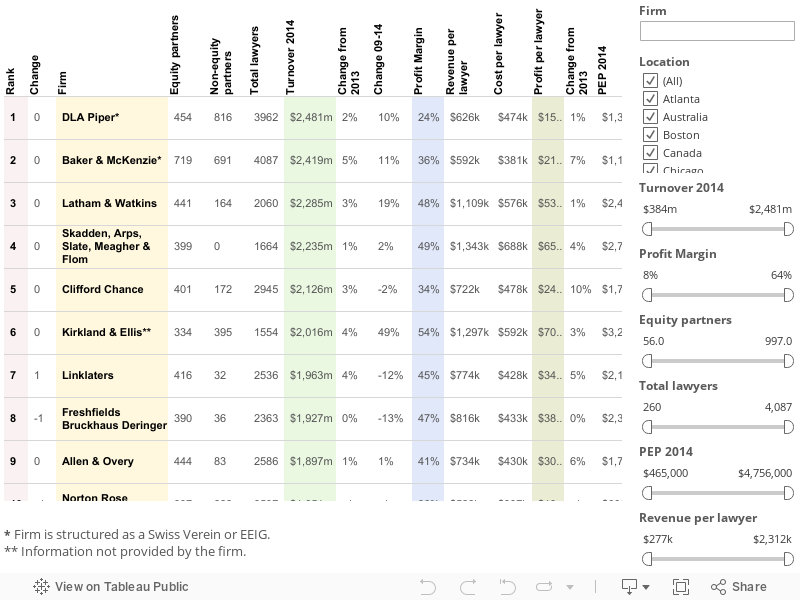

Comment: Marking your own homework, Dentons and a defence of PEP Law firms Legal Business 12 Jun 2014